Understanding Risk Is Where Better Portfolios Begin

Founded on a powerful observation from 40 years inside major investment banks: most investment mistakes start with not fully understanding the risk you already own.

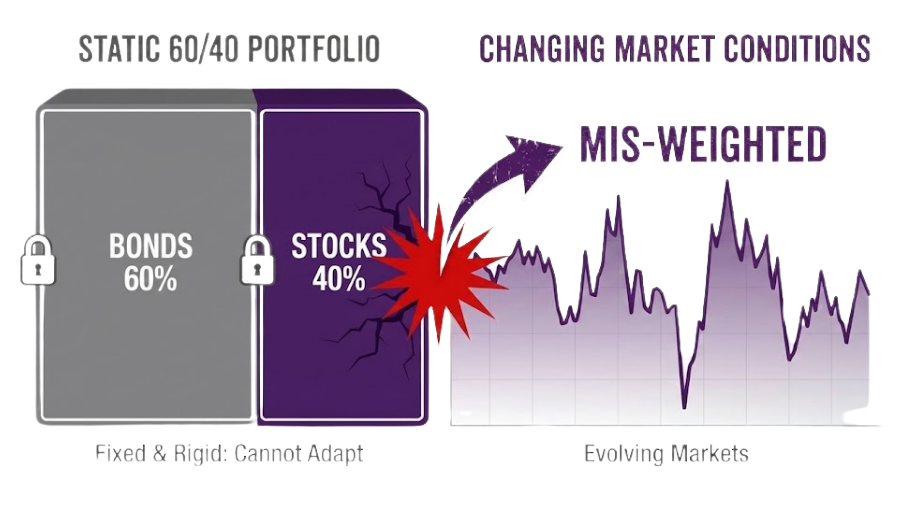

The Problem: The Risk Blind Spot

Most portfolios carry risk their owners cannot see. Correlated holdings, hidden factor crowding, and concentration that only surfaces during a drawdown.

Without analytics that show you what is actually driving your portfolio, weighting decisions are guesswork. And guesswork compounds into underperformance.

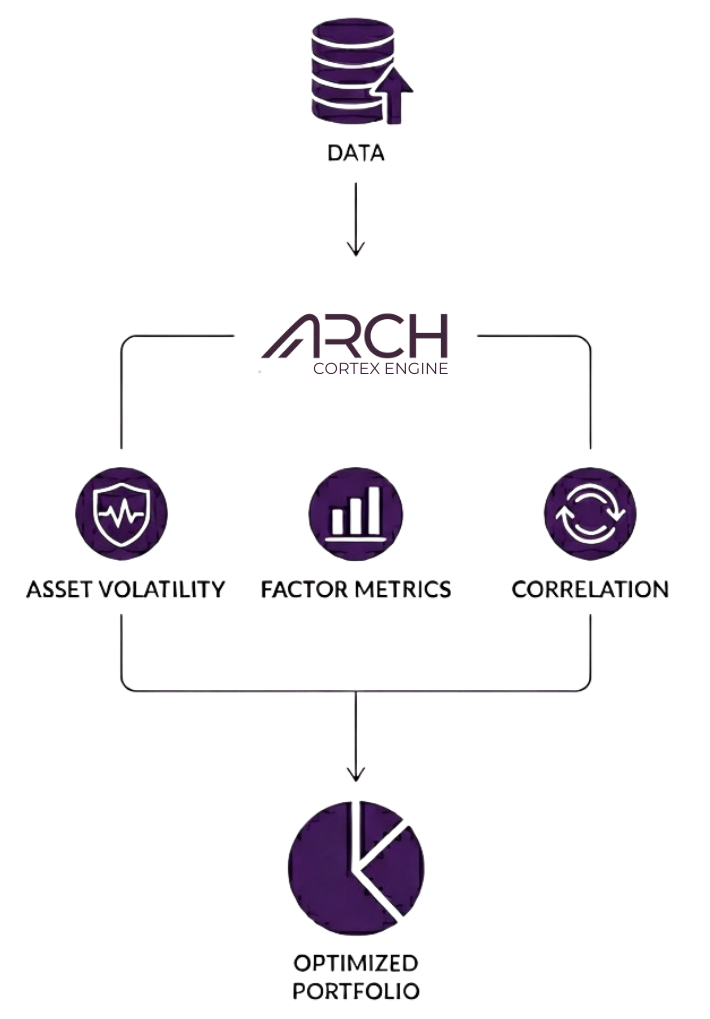

The Solution: See Risk, Rebuild Around It

Our analytics decompose any portfolio into factor exposures and risk attribution. So you see what you actually own before making any changes.

Then our Arch Cortex Engine (ACE) rebuilds the portfolio around the risk profile you want. Optimizing for your specific goals while minimizing uncompensated exposure.

Powered by proprietary machine learning and a recursive optimization framework built from decades of capital markets experience.

Our Founders: 40+ Years in Capital Markets

Yang Tang

Co-Founder & CEO

Yang is the CEO and a co-founder of Arch Analytics and Arch Indices.

Yang spent over a decade in macro solutions, structuring and sales roles at Morgan Stanley, Citi, Deutsche Bank, and Credit Agricole CIB. Yang has worked with banks, insurers, and asset managers globally on solutions across asset classes for asset liability, yield enhancement, capital, and tactical opportunities. These structured solutions combined advanced machine learning and derivative replication with practitioner knowledge of financial markets to achieve client outcomes.

Yang has earned a MBA from Columbia Business School and a BS in Economics from Purdue University. Prior to Columbia, Yang worked in research and commodities sales.

Dr. Jinghua "Jacob" Kuang

Co-Founder & CPO

Jacob is the CPO and a co-founder of Arch Analytics and Arch Indices.

Jacob spent over two decades at Citi and its predecessor Salomon Brothers in trading, structuring, and quantitative research/analytics. Jacob has deep expertise working with institutional and private bank clients in multi-asset derivative solutions, cash products, and structured notes. Jacob has extensive machine learning, neural network, financial engineering, and analytics knowledge from roles in research, modeling, and quantitative analysis in both cash products and derivatives.

Jacob has earned a PhD in Mathematics from the University of Minnesota and was an Assistant Professor of Mathematics at Penn State University.

Ready to See What's in Your Portfolio?

Let us show you how our analytics can reveal and optimize the risk in your holdings

Get in TouchDisclaimer

Copyright © 2025 by Arch Indices Corporation. All rights reserved. Arch Analytics and Arch Indices are a trademark of Arch Indices Corporation.

The content contained herein does not constitute an offer of investment services. All information provided is impersonal and not tailored to the needs of any person, entity or group of persons unless specifically licensed to do so. Information, indices, portfolios, and analytics provided by Arch Indices is solely for informational purposes.

An index or model portfolio is a hypothetical basket and cannot be invested in directly. Please consult your investment advisor for investment products that track indices or model portfolios.